Every lender has an online 1003. Some are good, and most are bad. I spend a lot of time evaluating online loan applications, and the following is what I've observed.

This article's format was inspired by Ben Horowitz's famous "Good Product Manager/Bad Product Manager" blog post.

Good 1003s are designed with borrowers in mind. They serve as a way for borrowers to get closer to their objective (pre-qualify, purchase a home, refinance, etc.) Bad 1003s aren't designed with the borrower in mind but instead serve as a way for the loan officer to get information into the LOS without entering it themselves.

Good 1003s enable borrowers to get the process started quickly by leading the borrower down their desired path with questions that a borrower would expect to be asked this early on. Conversely, bad 1003s force borrowers to "CREATE AN ACCOUNT!" before they've even had a chance to understand what's happening.

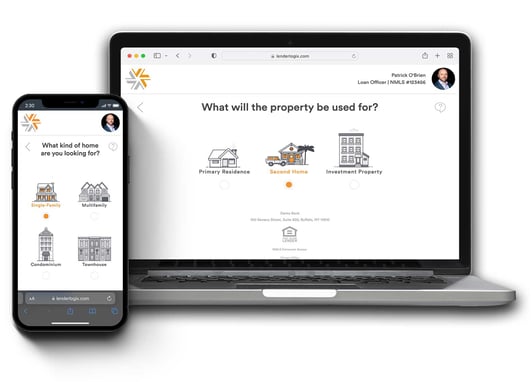

Good 1003s are interactive and fun and include design elements that elicit joy from the borrower. Bad 1003s look like tax return forms and elicit anxiety from the borrower.

Good 1003s get leads into the hands of the loan officers and data into the LOS immediately. Bad 1003s are a black hole and can't be relied upon to get the loan officer their leads.

Good 1003s demonstrate to prospects that the lender cares about the borrower's experience. Bad 1003s give borrowers a peek at how horrible the experience will be for the entire loan process.

Good 1003s don't need instruction manuals, they're intuitive and beautiful and give the borrower the feeling of a high-class experience. On the other hand, bad 1003s require loan officers to create how-to instructions for filing out the form, force borrowers to change browser settings, don't work on mobile devices, and give borrowers the feeling of an early 2000s website.

Good 1003s are optimized to capture leads for loan officers — bad 1003s cost loan officers business.

Good 1003s are an extension of the loan officer's white-glove service. Bad 1003s force loan officers to tell borrowers to avoid applying online because they know it will make them look bad.

LenderLogix created LiteSpeed to make Good 1003s the standard.

Currently available to Encompass® users, LiteSpeed guides borrowers through singular, auto-advancing application questions that boast animated iconography, dynamic messaging, and tasteful branding. Borrowers receive confirmation emails with their next steps, a secure document upload link, and more from their selected loan officer.

This type of high-touch early engagement is essential and shouldn't be hidden within an app or behind a login screen. Lenders using LiteSpeed see increased lead capture, increased applications, consistent brand identity across branches & teams, and more granular insight into marketing and sales performance.

While most POS solutions operate on a per-loan cost that rivals the LOS pricing, LiteSpeed can be implemented for about 90% less. In addition, it can be implemented within a week, includes unlimited customized training, and is backed by a 24x7 dedicated account manager and support team. This reduces the total cost of ownership for lenders and has ensured high adoption rates.

Let's Transform Your 1003

If you're looking to provide homebuyers with a simple yet amazing user experience, you should check out a live demonstration of LiteSpeed. Within 90 seconds, borrowers give the essential information needed to trigger a new loan within Encompass®.