Customer experience has emerged as a paramount aspect of success in the rapidly evolving mortgage industry. With the widespread adoption of digital mortgage technology and the highly competitive market, lenders are more pressured than ever to differentiate themselves, especially small and mid-sized lenders with constrained budgets.

However, not all technology-driven experiences are created equal. Merely implementing technology for the sake of it may not lead to improved customer satisfaction. Let’s delve into the importance of considering the borrower’s experience while adopting digital mortgage technology. Imagine walking into your favorite restaurant and being informed of a 30 to 35-minute wait for a table. You decide to stay and are asked for your phone number, with the promise of receiving a text when your table is available.

The first crucial aspect is the automatic text confirmation, assuring the customer that they are indeed on the waiting list. This immediate confirmation eliminates ambiguity, providing the diner peace of mind. Likewise, in the mortgage origination process, borrowers seek similar reassurance that their application has been received and is being processed.

Furthermore, the restaurant’s technology offers real-time updates, enabling customers to check their position in line relative to others. This transparency creates a sense of control and reduces the perceived waiting time. Similarly, in the mortgage process, borrowers appreciate having access to real-time updates about the status of their application, offering them confidence and minimizing anxiety.

Balancing Technology and Human Interaction

The implementation of technology in the restaurant example isn’t intended to replace the human touch but to complement it. By automating low-value tasks like managing the waiting list, restaurant hosts can focus on providing exceptional customer service. Likewise, in the mortgage industry, technology should empower loan officers to engage more effectively with borrowers, fostering a sense of personal connection and trust.

However, it is essential to strike the right balance between automation and human interaction. While digital mortgage solutions aim to streamline processes, they should never compromise on the personal touch borrowers expect.

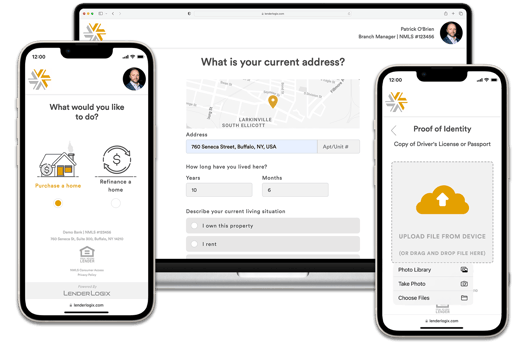

Point-of-Sale Solutions in Mortgage Origination

In today’s mortgage market, digital applications have become a prerequisite. However, having an online application is just the starting point. Point-of-sale (POS) solutions play a crucial role in the borrower’s journey as they are often the first interaction point between the borrower and the lender.

An effective POS solution should prioritize user experience and be designed with the borrower in mind. It should be intuitive, easy to navigate, and transparent, guiding borrowers through the application process seamlessly. Moreover, it should provide real-time status updates, allowing borrowers to stay informed throughout the journey.

As the mortgage industry embraces digital transformation, customer experience should remain at the heart of all technological implementations. The restaurant analogy illustrates the significance of providing borrowers with automated confirmations, real-time updates, and a balanced blend of technology and human interaction.

In mortgage origination, POS solutions are pivotal in shaping the borrower experience. However, their mere presence isn’t enough; they must be thoughtfully designed and combined with the right level of human engagement.

By understanding borrowers’ expectations and leveraging technology to enhance their experience, mortgage lenders can build trust, loyalty, and a competitive edge in the market. Ultimately, prioritizing customer experience in the digital mortgage era will lead to greater success for both borrowers and lenders alike.