As the spring homebuying season takes off, signs point to growing borrower momentum in the mortgage market. LenderLogix’s Q1 2025 Homebuyer Intelligence Report shows more homebuyers are getting pre-approved, moving faster from pre-approval to application, and staying actively engaged throughout the loan process. Based on data from LenderLogix’s digital solutions, the report highlights how the industry is embracing technology to navigate a competitive market with confidence and enable better, faster, impactful borrower interactions.

Pre-Approval Activity Picks Up

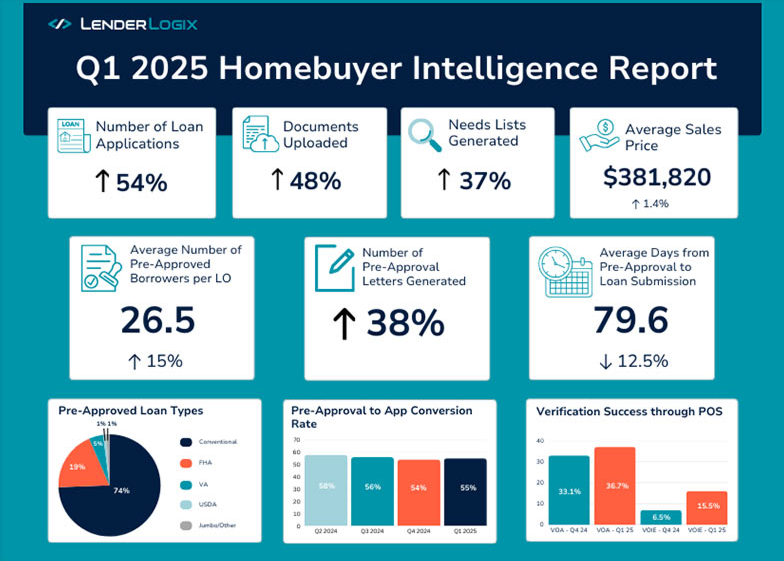

Homebuyer engagement surged to start the year. In Q1 2025, pre-approval letters generated through LenderLogix’s QuickQual platform increased nearly 38% over the previous quarter, a clear sign that buyers are entering the market prepared and with purpose.

Loan officers also saw an increase in borrower activity, averaging 26.5 pre-approved clients each, up from 23 in Q4 2024. That boost in engagement matters: it signals growing consumer confidence and a more competitive purchase environment, where speed and readiness can make all the difference.

While the average loan amount and down payment ticked up slightly, the real story is how borrowers are strategically taking advantage of digital pre-approval tools. They’re getting pre-approved earlier and using quickly generated letters such as those powered by QuickQual to move fast, an essential edge in today’s market.

Conversion Rates Climb as Homebuyers Move Decisively

Beyond early engagement, homebuyers are also moving more decisively. In Q1 2025, the average time between pre-approval and loan application dropped from 91 days to just under 80. That shift signals a subtle yet important change in borrower behavior: buyers are motivated and ready to act.

QuickQual’s borrower conversion rate also rose slightly, from 54% to 55%. Borrowers continued to generate an average of eight pre-approval letters before applying, underscoring how they're using pre-approvals to stay nimble in a dynamic market.

This pace is matched by increased lender responsiveness. Applications submitted through LenderLogix’s LiteSpeed platform rose 54% over Q4, indicating that lenders are not just keeping up with borrower expectations but helping drive momentum forward.

“Pre-approvals are a key signal of consumer intentions, and we’re seeing homebuying intent grow stronger,” said LenderLogix Co-Founder and CEO Patrick O’Brien. “Not only are more buyers getting pre-approved, but they’re also moving from pre-approval to application faster. That tells us they’re not just window shopping—they’re serious, strategic, and ready to compete.”

Post-Application Activity Points to Deeper Engagement

The signs of borrower momentum didn’t stop at application. In Q1 2025, document uploads through the LiteSpeed platform increased 48% from Q4. This uptick suggests borrowers are increasingly active and responsive during the loan process.

Supporting that trend, the number of “Needs Lists” created—customized checklists of required documents and steps—rose significantly by 37%. Borrowers are staying on track, and lenders are clearly equipping them with better tools to do so.

Digital verification rates also improved. Successful verification of income and employment more than doubled from 6.5% to 15.1%, and verification of assets increased from 33.1% in Q4 to 36.7% in Q1. These improvements streamline the loan process, enabling faster underwriting and stronger loan files.

Final Thoughts: Tools That Turn Momentum Into Results

As the data from Q1 2025 shows, today’s homebuyers are coming to the table better prepared, more decisive, and more engaged than before. That level of momentum doesn’t happen on its own; it’s powered by technology that simplifies the mortgage process and meets borrowers where they are.

From early-stage pre-approvals to post-application document uploads and verifications, LenderLogix’s suite of tools, including QuickQual, Fee Chaser, and LiteSpeed, are helping lenders keep pace with buyer expectations and deliver experiences that build trust and drive results.

In a competitive market, that kind of engagement matters. It means fewer delays, confident lending decisions, and a smoother path to the closing table for everyone involved.